Thursday, 16-Jul-2026 NIFTY: --% | SENSEX: --%

A mutual fund is a pool of money managed by a professional Fund Manager.

It is a trust that collects money from several investors who share a common investment objective and invests the same in equities, bonds, money market instruments and/or other securities. And the income / gains generated from this collective investment is distributed proportionately amongst the investors after deducting applicable expenses and levies, by calculating a scheme’s “Net Asset Value” or NAV. Simply put, the money pooled in by many investors is what makes up a Mutual Fund.

Here’s a simple way to understand the concept of a Mutual Fund Unit. Let’s say that there is a box of 12 chocolates costing ₹40. Four friends decide to buy the same, but they have only ₹10 each and the shopkeeper only sells by the box. So, the friends then decide to pool in ₹10 each and buy the box of 12 chocolates. Now based on their contribution, they each receive 3 chocolates or 3 units, if equated with Mutual Funds.

And how do you calculate the cost of one unit? Simply divide the total amount with the total number of chocolates: 40/12 = 3.33. So if you were to multiply the number of units (3) with the cost per unit (3.33), you get the initial investment of ₹10.

This results in each friend being a unit holder in the box of chocolates that is collectively owned by all of them, with each person being a part owner of the box.

Next, let us understand what “Net Asset Value” or NAV is. Just like an equity share has a traded price, a mutual fund unit has Net Asset Value per Unit. The NAV is the combined market value of the shares, bonds and securities held by a fund on any day (as reduced by permitted expenses and charges). NAV per Unit represents the market value of all the Units in a mutual fund scheme on a given day, net of all expenses and liabilities plus income accrued, divided by the outstanding number of Units in the scheme.

Mutual funds are ideal for investors who either lack large sums for investment, or for those who neither have the inclination nor the time to research the market yet want to grow their wealth. The money collected in mutual funds is invested by professional fund managers in line with the scheme’s stated objective. In return, the fund house charges a small fee which is deducted from the investment. The fees charged by mutual funds are regulated and are subject to certain limits specified by the Securities and Exchange Board of India (SEBI).

Mutual funds offer multiple product choices for investment across the financial spectrum. As investment goals vary – post-retirement expenses, money for children’s education or marriage, house purchase, etc. – the products required to achieve these goals vary too. The Indian mutual fund industry offers a plethora of schemes and caters to all types of investor needs.

Mutual funds offer an excellent avenue for retail investors to participate and benefit from the uptrends in capital markets. While investing in mutual funds can be beneficial, selecting the right fund can be challenging. Hence, investors should do proper due diligence of the fund and take into consideration the risk- return trade-off and time horizon or consult a professional investment adviser. Further, to reap maximum benefit from mutual fund investments, it is important for investors to diversify across different categories of funds such as equity, debt and gold.

While investors of all categories can invest in securities market on their own, a mutual fund is a better choice for the only reason that all benefits come in a package.

Mutual funds are favoured globally for the variety of investment options they offer. There is something for every profile and preference.

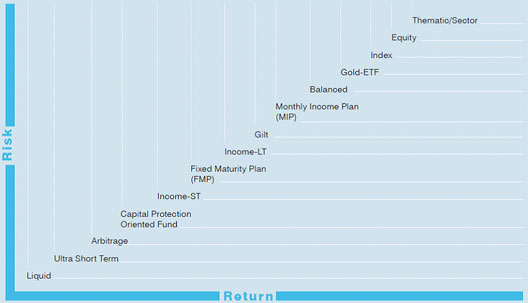

Chart 1: Risk/Return trade-off by mutual fund category

Mutual Fund schemes could be ‘open ended’ or close-ended’ and actively managed or passively managed.

An open-end fund is a mutual fund scheme that is available for subscription and redemption on every business throughout the year, (akin to a savings bank account, wherein one may deposit and withdraw money every day). An open- ended scheme is perpetual and does not have any maturity date.

A closed-end fund is open for subscription only during the initial offer period and has a specified tenor and fixed maturity date (akin to a fixed term deposit). Units of Closed-end funds can be redeemed only on maturity (i.e., pre-mature redemption is not permitted). Hence, the Units of a closed-end fund are compulsorily listed on a stock exchange after the new fund offer and are traded on the stock exchange just like other stocks, so that investors seeking to exit the scheme before maturity may sell their Units on the exchange.

An actively managed fund is a mutual fund scheme in which the fund manager “actively” manages the portfolio and continuously monitors the fund's portfolio, deciding on which stocks to buy/sell/hold and when, using his professional judgement, backed by analytical research. In an active fund, the fund manager’s aim is to generate maximum returns and out-perform the scheme’s benchmark.

A passively managed fund, by contrast, simply follows a market index, i.e., in a passive fund, the fund manager remains inactive or passive in as much as, she does not use her judgement or discretion to decide as to which stocks to buy/sell/hold, but simply replicates / tracks the scheme’s benchmark index in the same proportion. Examples of Index funds are an Index Fund and all Exchange Traded Funds. In a passive fund, the fund manager’s task is to simply replicate the scheme’s benchmark index i.e., generate the same returns as the index, and not to out-perform the scheme’s benchmark.

1. Professional Management — Investors may not have the time or the required knowledge and resources to conduct their research and purchase individual stocks or bonds. A mutual fund is managed by full-time, professional money managers who have the expertise, experience, and resources to actively buy, sell, and monitor investments. A fund manager continuously monitors investments and rebalances the portfolio accordingly to meet the scheme’s objectives. Portfolio management by professional fund managers is one of the most important advantages of a mutual fund.

2. Risk Diversification — Buying shares in a mutual fund is an easy way to diversify your investments across many securities and asset categories such as equity, debt, and gold, which helps in spreading the risk - so you won't have all your eggs in one basket. This proves to be beneficial when an underlying security of a given mutual fund scheme experiences market headwinds. With diversification, the risk associated with one asset class is countered by the others. Even if one investment in the portfolio decreases in value, other investments may not be impacted and may even increase in value. In other words, you don’t lose out on the entire value of your investment if a particular component of your portfolio goes through a turbulent period. Thus, risk diversification is one of the most prominent advantages of investing in mutual funds.

3. Affordability & Convenience (Invest Small Amounts) — For many investors, it could be more costly to directly purchase all the individual securities held by a single mutual fund. By contrast, the minimum initial investments for most mutual funds are more affordable.

4. Liquidity — You can easily redeem (liquidate) units of open-ended mutual fund schemes to meet your financial needs on any business day (when the stock markets and/or banks are open), so you have easy access to your money. Upon redemption, the redemption amount is credited in your bank account within one day to 3-4 days, depending upon the type of scheme e.g., in respect of Liquid Funds and Overnight Funds, the redemption amount is paid out the next business day.

However, please note that units of close-ended mutual fund schemes can be redeemed only on maturity. Likewise, units of ELSS have a 3-year lock-in period and can be liquidated only thereafter.

5. Low Cost — An important advantage of mutual funds is their low cost. Due to huge economies of scale, mutual funds schemes have a low expense ratio. Expense ratio represents the annual fund operating expenses of a scheme, expressed as a percentage of the fund’s daily net assets. Operating expenses of a scheme are administration, management, advertising related expenses, etc. The limits of expense ratio for various types of schemes have been specified under Regulation 52 of SEBI Mutual Fund Regulations, 1996.

6. Well-Regulated —Mutual Funds are regulated by the capital markets regulator, Securities and Exchange Board of India (SEBI) under SEBI (Mutual Funds) Regulations, 1996. SEBI has laid down stringent rules and regulations keeping investor protection, transparency with appropriate risk mitigation framework and fair valuation principles.

7. Tax Benefits — Investment in ELSS up to ₹1,50,000 qualifies for tax benefit under section 80C of the Income Tax Act, 1961. Mutual Fund investments when held for a longer term are tax efficient.

As per SEBI guidelines on Categorization and Rationalization of schemes issued in October 2017, mutual fund schemes are classified as –

An equity Scheme is a fund that –

– Primarily invests in equities and equities related instruments. defined.

– Seeks long term growth but could be volatile in the short term.

– Suitable for investors with higher risk appetite and longer investment horizon.

The objective of an equity fund is generally to seek long-term capital appreciation. Equity funds may focus on certain sectors of the market or may have a specific investment style, such as investing in value or growth stocks.

| Multi Cap Fund* | At least 65% investment in equity & equity related instruments |

| Large Cap Fund | At least 80% investment in large cap stocks |

| Large & Mid Cap Fund | At least 35% investment in large cap stocks and 35% in mid cap stocks |

| Mid Cap Fund | At least 65% investment in mid cap stocks |

| Small cap Fund | At least 65% investment in small cap stocks |

| Dividend Yield Fund | Predominantly invest in dividend yielding stocks, with at least 65% in stocks |

| Value Fund | Value investment strategy, with at least 65% in stocks |

| Contra Fund | Scheme follows contrarian investment strategy with at least 65% in stocks |

| Focused Fund | Focused on the number of stocks (maximum 30) with at least 65% in equity & equity related instruments |

| Sectoral/ Thematic Fund | At least 80% investment in stocks of a particular sector/ theme |

| ELSS | At least 80% in stocks in accordance with Equity Linked Saving Scheme, 2005, notified by Ministry of Finance |

*Also referred to as Diversified Equity Funds – as they invest across stocks of different sectors and segments of the market. Diversification minimizes the risk of high exposure to a few stocks, sectors, or segment.

Sectoral funds invest in a particular sector of the economy such as infrastructure, banking, technology, or pharmaceuticals etc.

– Since these funds focus on just one sector of the economy, they limit diversification, and are thus riskier.

– Timing of investment into such funds are important because the performance of the sectors tend to be cyclical.

Examples of Sector Specific Funds - Equity Mutual Funds with an investment objective to invest in

● Pharma & Healthcare Sector

● Banking & Finance Sector.

● FMCG (fast moving consumer goods) and related sectors.

● Technology and related sectors

● Thematic funds select stocks of companies in industries that belong to a particular theme - For example, Infrastructure, Service industries, PSUs or MNCs.

● They are more diversified than Sectoral Funds and hence have lower risk than Sectoral funds.

● Equity funds may be categorized based on the valuation parameters adopted in stock selection, such as

– Growth funds identify momentum stocks that are expected to perform better than the market

– Value funds identify stocks that are currently undervalued but are expected to perform well over time as the value is unlocked

● Equity funds may hold a concentrated portfolio to benefit from stock selection.

– These funds will have a higher risk since the effect of a wrong selection can be substantial on the portfolio’s return

● Contra funds are equity mutual funds that take a contrarian view on the market.

● Underperforming stocks and sectors are picked at low price points with a view that they will perform in the long run.

● The portfolios of contra funds have defensive and beaten down stocks that have given negative returns during bear markets.

● These funds carry the risk of getting calls wrong as catching a trend before the herd is not possible in every market cycle and these funds typically underperform in a bull market.

● As per the SEBI guidelines on Scheme categorisation of mutual funds, a fund house can either offer a Contra Fund or a Value Fund, not both.

ELSS invests at least 80% in stocks in accordance with Equity Linked Saving Scheme, 2005, notified by Ministry of Finance.

● Has lock-in period of 3 years (which is shortest amongst all other tax saving options)

● Currently eligible for deduction under Sec 80C of the Income Tax Act up to ₹1,50,000

● A debt fund (also known as income fund) is a fund that invests primarily in bonds or other debt securities.

● Debt funds invest in short and long-term securities issued by government, public financial institutions, companies.

– Treasury bills, Government Securities, Debentures, Commercial paper, Certificates of Deposit, and others.

● Debt funds can be categorized based on the tenor of the securities held in the portfolio and/or based on the issuers of the securities or their fund management strategies, such as

– Short-term funds, Medium-term funds, Long-term funds

– Gilt fund, Treasury fund, corporate bond fund, Infrastructure debt fund

● Floating rate funds, Dynamic Bond funds, Fixed Maturity Plans

● Debt funds have potential for income generation and capital preservation.

| Overnight Fund | Overnight securities having maturity of 1 day |

| Liquid Fund | Debt and money market securities with maturity of up to 91 days only |

| Ultra Short Duration Fund | Debt & Money Market instruments with Macaulay duration of the portfolio between 3 months - 6 months |

| Low Duration Fund | Investment in Debt & Money Market instruments with Macaulay duration portfolio between 6 months- 12 months |

| Money Market Fund | Investment in Money Market instruments having maturity up to 1 Year |

| Short Duration Fund | Investment in Debt & Money Market instruments with Macaulay duration of the portfolio between 1 year - 3 years |

| Medium Duration Fund | Investment in Debt & Money Market instruments with Macaulay duration of portfolio between 3 years - 4 years |

| Medium to Long Duration Fund | Investment in Debt & Money Market instruments with Macaulay duration of the portfolio between 4 - 7 years |

| Long Duration Fund | Investment in Debt & Money Market Instruments with Macaulay duration of the portfolio greater than 7 years |

| Dynamic Bond | Investment across duration |

| Corporate Bond Fund | Minimum 80% investment in corporate bonds only in AA+ and above rated corporate bonds |

| Credit Risk Fund | Minimum 65% investment in corporate bonds, only in AA and below rated corporate bonds |

| Banking and PSU Fund | Minimum 80% in Debt instruments of banks, Public Sector Undertakings, Public Financial Institutions and Municipal Bonds |

| Gilt Fund | Minimum 80% in G-secs, across maturity |

| Gilt Fund with 10- year constant Duration | Minimum 80% in G-secs, such that the Macaulay duration of the portfolio is equal to 10 years |

| Floater Fund | Minimum 65% in floating rate instruments (including fixed rate instruments converted to floating rate exposures using swaps/ derivatives) |

Dynamic Bond funds alter the tenor of the securities in the portfolio in line with expectation on interest rates. The tenor is increased if interest rates are expected to go down and vice versa.

Floating rate funds invest in bonds whose interest are reset periodically so that the fund earns coupon income that is in line with current rates in the market and eliminates interest rate risk to a large extent.

The primary focus of short-term debt funds is coupon income. Short term debt funds must also be evaluated for the credit risk they may take to earn higher coupon income. The tenor of the securities will define the return and risk of the fund.

– Funds holding securities with lower tenors have lower risk and lower return.

● Liquid funds invest in securities with not more than 91 days to maturity.

● Ultra Short-Term Debt Funds hold a portfolio with a slightly higher tenor to earn higher coupon income.

Short-Term Fund combine coupon income earned from a pre-dominantly short- term debt portfolio with some exposure to longer term securities to benefit from appreciation in price.

– FMPs are closed-ended funds which eliminate interest rate risk and lock-in a yield by investing only in securities whose maturity matches the maturity of the fund.

– FMPs create an investment portfolio whose maturity profile match that of the FMP tenor.

– Potential to provide better returns than liquid funds and Ultra Short-Term Funds since investments are locked in

– Low mark to market risk as investments are liquidated at maturity.

– Investors commit money for a fixed period.

– Investors cannot prematurely redeem the units from the fund

– FMPs, being closed-end schemes are mandatorily listed - investors can buy or sell units of FMPs only on the stock exchange after the NFO.

– Only Units held in dematerialized mode can be traded; therefore, investors seeking liquidity in such schemes need to have a demat account. Capital Protection Oriented Funds Capital Protection Oriented Funds are close-ended hybrid funds that create a portfolio of debt instruments and equity derivatives.

– The portfolio is structured to provide capital protection and is rated by a credit rating agency on its ability to do so. The rating is reviewed every quarter.

– The debt component of the portfolio must be invested in instruments with the highest investment grade rating.

– A portion of the amount brought in by the investors is invested in debt instruments that is expected to mature to the par value of the capital invested by investors into the fund. The capital is thus protected.

– The remaining portion of the funds is used to invest in equity derivatives to generate higher returns.

Hybrid funds Invest in a mix of equities and debt securities.

SEBI has classified Hybrid funds into 7 sub-categories as follows:

| Conservative Hybrid Fund | 10% to 25% investment in equity & equity related instruments; and 75% to 90% in Debt instruments |

| Balanced Hybrid Fund | 40% to 60% investment in equity & equity related instruments; and 40% to 60% in Debt instruments |

| Aggressive Hybrid Fund | 65% to 80% investment in equity & equity related instruments; and 20% to 35% in Debt instruments |

| Dynamic Asset Allocation or Balanced Advantage Fund | Investment in equity/ debt that is managed dynamically (0% to 100% in equity & equity related instruments; and 0% to 100% in Debt instruments) |

| Multi Asset Allocation Fund | Investment in at least 3 asset classes with a minimum allocation of at least 10% in each asset class |

| Arbitrage Fund | Scheme following arbitrage strategy, with minimum 65% investment in equity & equity related instruments |

| Equity Savings | Equity and equity related instruments (min.65%); debt instruments (min.10%) and derivatives (min. for hedging to be specified in the SID) |

| Retirement Fund | Lock-in for at least 5 years or till retirement age whichever is earlier |

| Children’s Fund | Lock-in for at least 5 years or till the child attains age of majority whichever is earlier |

| Index Funds/ ETFs | Minimum 95% investment in securities of a particular index |

| Fund of Funds (Overseas/ Domestic) | Minimum 95% investment in the underlying fund(s) |

Invest in a mix of equities and debt securities. They seek to find a ‘balance’ between growth and income by investing in both equity and debt.

– The regular income earned from the debt instruments provide greater stability to the returns from such funds.

– The proportion of equity and debt that will be held in the portfolio is indicated in the Scheme Information Document

– Equity oriented hybrid funds (Aggressive Hybrid Funds) are ideal for investors looking for growth in their investment with some stability.

– Debt-oriented hybrid funds (Conservative Hybrid Fund) are suitable for conservative investors looking for a boost in returns with a small exposure to equity.

– The risk and return of the fund will depend upon the equity exposure taken by the portfolio - Higher the allocation to equity, greater is the risk

● A multi-asset fund offers exposure to a broad number of asset classes, often offering a level of diversification typically associated with institutional investing.

● Multi-asset funds may invest in a number of traditional equity and fixed income strategies, index-tracking funds, financial derivatives as well as commodity like gold.

● This diversity allows portfolio managers to potentially balance risk with reward and deliver steady, long-term returns for investors, particularly in volatile markets.

“Arbitrage” is the simultaneous purchase and sale of an asset to take advantage of the price differential in the two markets and profit from price difference of the asset on different markets or in different forms.

● Arbitrage fund buys a stock in the cash market and simultaneously sells it in the Futures market at a higher price to generate returns from the difference in the price of the security in the two markets.

● – The fund takes equal but opposite positions in both the markets, thereby locking in the difference.

● – The positions must be held until expiry of the derivative cycle and both positions need to be closed at the same price to realize the difference.

● – The cash market price converges with the Futures market price at the end of the contract period. Thus, it delivers risk-free profit for the investor/trader.

● – Price movements do not affect initial price differential because the profit in one market is set-off by the loss in the other market.

● – Since mutual funds invest own funds, the difference is fully the return.

Hence, Arbitrage funds are a good choice for cautious investors who want to benefit from a volatile market without taking on too much risk.

Index funds create a portfolio that mirrors a market index.

● – The securities included in the portfolio and their weights are the same as that in the index

● – The fund manager does not rebalance the portfolio based on their view of the market or sector

● – Index funds are passively managed, which means that the fund manager makes only minor, periodic adjustments to keep the fund in line with its index. Hence, Index fund offers the same return and risk represented by the index it tracks.

● – The fees that an index fund can charge is capped at 1.5%

Investors have the comfort of knowing the stocks that will form part of the portfolio, since the composition of the index is known.

An ETF is a marketable security that tracks an index, a commodity, bonds, or a basket of assets like an index fund.

● ETFs are listed on stock exchanges.

● Unlike regular mutual funds, an ETF trades like a common stock on a stock exchange. The traded price of an ETF changes throughout the day like any other stock, as it is bought and sold on the stock exchange.

● ETF Units are compulsorily held in Demat mode.

● ETFs are passively managed, which means that the fund manager makes only minor, periodic adjustments to keep the fund in line with its index.

● Because an ETF tracks an index without trying to outperform it, it incurs lower administrative costs than actively managed portfolios.

● Rather than investing in an ‘active’ fund managed by a fund manager, when one buy units of an ETF one is harnessing the power of the market itself.

● Suitable for investors seeking returns similar to index and liquidity similar to stocks.

● Fund of funds are mutual fund schemes that invest in the units of other schemes of the same mutual fund or other mutual funds.

● The schemes selected for investment will be based on the investment objective of the FoF

● The FoF have two levels of expenses: that of the scheme whose units the FoF invests in and the expense of the FoF itself. Regulations limit the total expenses that can be charged across both levels as follows:

– TER in respect of FoF investing liquid schemes, index funds & ETFs has been capped @ 1%

– TER of FoF investing in equity-oriented schemes has been capped @ 2.25%

– TER of FoF investing in other schemes than mentioned above has been capped @2%.

● Gold ETFs are ETFs with gold as the underlying asset.

– The scheme will issue units against gold held. Each unit will represent a defined weight in gold, typically one gram.

– The scheme will hold gold in form of physical gold or gold related instruments approved by SEBI.

– Schemes can invest up to 20% of net assets in Gold Deposit Scheme of banks.

● The price of ETF units moves in line with the price of gold on metal exchange.

● After the NFO, units are issued to intermediaries called authorized participants against gold or funds submitted. They can also redeem the units for the underlying gold.

● Convenience --> option of holding gold electronically instead of physical gold.

– Safer option to hold gold since there are no risks of theft or purity.

– Provides easy liquidity and ease of transaction.

● Gold ETFs are treated as non-equity oriented mutual funds for the purpose of taxation.

– Eligible for long-term capital gains benefits if held for three years.

– No wealth tax is applicable on Gold ETFs

International funds enable investments in markets outside India, by holding in their portfolio one or more of the following :

● Open-ended schemes are perpetual, and open for subscription and repurchase on a continuous basis on all business days at the current NAV.

● Close-ended schemes have a fixed maturity date. The units are issued at the time of the initial offer and redeemed only on maturity. The units of close-ended schemes are mandatorily listed to provide exit route before maturity and can be sold/traded on the stock exchanges.

● Interval schemes allow purchase and redemption during specified transaction periods (intervals). The transaction period must be for a minimum of 2 days and there should be at least a 15-day gap between two transaction periods. The units of interval schemes are also mandatorily listed on the stock exchanges.

In an Active Fund, the Fund Manager is ‘Active’ in deciding whether to Buy, Hold, or Sell the underlying securities and in stock selection. Active funds adopt different strategies and styles to create and manage the portfolio.

● The investment strategy and style are described upfront in the Scheme Information document (offer document)

● Active funds expect to generate better returns (alpha) than the benchmark index.

● The risk and return in the fund will depend upon the strategy adopted.

● Active funds implement strategies to ‘select’ the stocks for the portfolio.

Passive Funds hold a portfolio that replicates a stated Index or Benchmark e.g. –

● Index Funds

● Exchange Traded Funds (ETFs)

In a Passive Fund, the fund manager has a passive role, as the stock selection / Buy, Hold, sell decision is driven by the Benchmark Index and the fund manager / dealer merely needs to replicate the same with minimal tracking error.

Mutual funds offer products that cater to the different investment objectives of the investors such as –

a. Capital Appreciation (Growth)

b. Capital Preservation

c. Regular Income

d. Liquidity

e. Tax-Saving

Mutual funds also offer investment plans, such as Growth and Dividend options, to help tailor the investment to the investors’ needs.

● Growth Funds are schemes that are designed to provide capital appreciation.

● Primarily invest in growth-oriented assets, such as equity.

● Investment in growth-oriented funds require a medium to long-term investment horizon.

● Historically, Equity as an asset class has outperformed most other kind of investments held over the long term. However, returns from Growth funds tend to be volatile over the short-term since the prices of the underlying equity shares may change.

● Hence investors must be able to take volatility in the returns in the short- term.

A strong financial market with broad participation is essential for a developed economy. With this broad objective, India’s first mutual fund was established in 1963, namely, Unit Trust of India (UTI), at the initiative of the Government of India and Reserve Bank of India ‘with a view to encouraging saving and investment and participation in the income, profits and gains accruing to the Corporation from the acquisition, holding, management and disposal of securities.’

In the last few years, the MF Industry has grown significantly. Taking cognisance of the lack of penetration of MFs, especially in tier II and tier III cities, and the need for greater alignment of the interest of various stakeholders, SEBI introduced several progressive measures in September 2012 to "re-energize" the Indian Mutual Fund industry and increase MFs’ penetration.

In due course, the measures did succeed in reversing the negative trend that had set in after the global melt-down and improved significantly after the new Government was formed at the Centre. Since May 2014, the Industry has witnessed steady inflows and increase in the AUM as well as the number of investor folios (accounts).

● The Industry’s AUM crossed the milestone of ₹10 Trillion (₹10 Lakh Crore) for the first time as on 31st May 2014 and in a short span of about three years the AUM size had increased more than two folds and crossed ₹20 trillion (₹20 Lakh Crore) for the first time in August 2017. The AUM size crossed ₹30 trillion (₹30 Lakh Crore) for the first time in November 2020.

● The overall size of the Indian MF Industry has grown from ₹7.01 trillion as on 31st March 2013 to ₹39.42 trillion as on 31st March 2023, more than 5-fold increase in a span of 10 years.

● The MF Industry’s AUM has grown from ₹21.36 trillion as on March 31, 2018, to ₹39.42 trillion as on March 31, 2023, around 2-fold increase in a span of 5 years.

● The number of investor folios has gone up from 7.13 crore folios as on 31-Mar-2018 to 14.57 crore as on 31-Mar-2023, more than 2-fold increase in a span of 5 years.

● On average, 12.40 lakh new folios are added every month in the last 5 years since February 2018.

The growth in the size of the industry has been possible due to the twin effects of the regulatory measures taken by SEBI in re-energising the MF Industry in September 2012 and the support from mutual fund distributors in expanding the retail base.

MF Distributors have been providing the much-needed last mile connect with investors, particularly in smaller towns and this is not limited to just enabling investors to invest in appropriate schemes, but also in helping investors stay on course through bouts of market volatility and thus experience the benefit of investing in mutual funds.

MF distributors have also had a major role in popularising Systematic Investment Plans (SIP) over the years. In April 2016, the number of SIP accounts crossed the 1 crore mark and as on 31st March 2023 the total number of SIP Accounts stood at 6.36 crore.

Start Your Investing journey today by signing up with Indian Investment Services.

Happy Investing 😊

Redefine your wealth.

Redefine your wealth.